Kazakhstan Temir Joly in Debt — But Posts a Profit. How Did That Happen?

Photo: Midjorney Generated, ill. purposes

Photo: Midjorney Generated, ill. purposes

Kazakhstan’s national railway company, Kazakhstan Temir Joly (KTZ), has published its 2024 audit report, revealing a complex mix of numbers, Orda.kz reports.

KTZ remains deeply in debt: 3.9 trillion tenge as of the end of 2024, up from 3.1 trillion the previous year. Auditors highlight the company’s strong dependence on government support. Notably, KTZ’s total assets still don’t cover its total liabilities.

As of December 31, 2024, the group's current liabilities exceed current assets by 929,438 million tenge (December 31, 2023: 422,786 million tenge). As of the same date, current liabilities include loans totaling 812,965 million tenge, which are due within 12 months, including 460,805 million tenge in loans from the shareholder. At the same time, profit for the year ended December 31, 2024, amounted to 160,805 million tenge, and operating cash flow totaled 336,597 million tenge,the report states.

Total revenue reached 948 billion tenge, up 89 billion from 2023. Most of it came from cargo transport. Net profit grew to 160 billion tenge, up from 136 billion the year before.

KTZ also repaid two loans from Halyk Bank early, totaling 70 billion tenge.

Still, the company faces serious issues: a heavy debt load and significant wear and tear on its tracks and rolling stock.

Despite this, it remains profitable — and has even increased spending on holidays and entertainment.

State Loans, Under a Different Name

KTZ issued bonds three times in 2024:

- To upgrade the Dostyq–Moiynty line: Bonds issued in June and December totaled 20.3 billion and 143.6 billion tenge. Repayment is due by 2044, with a low interest rate of 9.25% — well below the market average of 12–14%. Auditors made a fair value adjustment. The difference — nearly 49.5 billion tenge — was recorded as a shareholder contribution, meaning it was treated as a kind of state subsidy rather than debt. These bonds were issued in digital tenge.

- To build the Darbaza–Maktaaral line: Bonds worth 44.2 billion tenge were issued in July 2024 at an extremely low rate of 1.8% (compared to the market rate of 12.3%). Auditors once again made a fair value adjustment: 33.9 billion tenge was written off to capital, since such a low rate can be interpreted as a form of government support rather than a standard market loan.

- To refinance old debt: In December 2024, KTZ issued 30 billion tenge in bonds at the National Bank’s base rate +0.75% — a more typical market loan.

In all cases, these bonds were not bought by private investors, but by the sole shareholder: the state, via the Samruq-qazyna National Welfare Fund.

In other words, KTZ received substantial funding at preferential rates — in some cases, almost interest-free.

The difference between the “preferential” and “market” value was recorded by the company as an additional shareholder contribution, not as debt. This reduces reported interest costs and improves the company’s financial appearance — but it’s still government financing, just dressed differently.

Railcars for Rent?

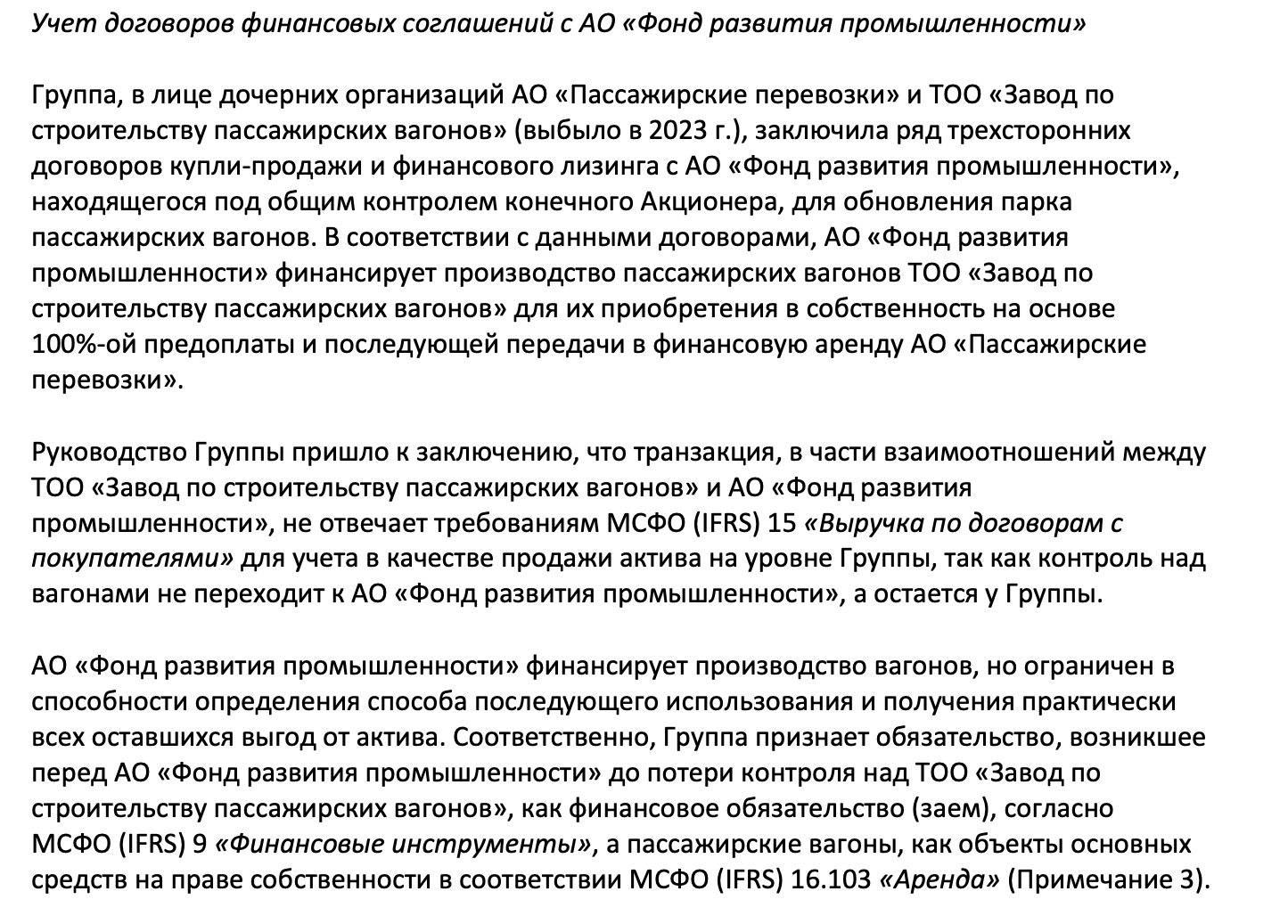

Auditors also reviewed KTZ’s controversial deal with Swiss manufacturer Stadler, previously covered by Orda.kz.

The cars are being assembled at Passenger Car Construction Plant LLP — a company that was first loaded with contracts worth 735 billion tenge and then transferred to Swiss company Stadler.

Since KTZ lacked the funds to fulfill the contract, it secured a loan from the Industrial Development Fund (IDF).

On paper, the transaction was structured to look as if the IDF bought the cars and then leased them to KTZ.

However, under International Financial Reporting Standards (IFRS), this arrangement cannot be recorded as a sale. That means KTZ cannot report revenue from a supposed sale. Instead, it must treat the transaction as a loan from the IDF.

The passenger cars, in turn, must be recorded as KTZ’s own assets, not as leased property.

Industrial Development Fund JSC is providing financing for the production of passenger railcars, but does not retain control over the manner of their subsequent use or the ability to derive substantially all of the economic benefits from the assets. Accordingly, the group recognizes the resulting obligation to Industrial Development Fund JSC— incurred prior to the loss of control over Passenger Car Construction Plant LLP — as a financial liability (loan) in accordance with IFRS 9 Financial Instruments. The passenger railcars themselves are recognized as property under the group’s ownership, in accordance with applicable IFRS standards,the report states.

Taxes and Executive Compensation

Even auditors admit they don’t fully grasp the intricacies of Kazakhstan’s tax system.

They warn that although the company has assessed its tax risks and set aside reserves, the actual penalties could end up being significantly higher, which could negatively affect future financial performance.

Various Kazakh laws and regulations are not always written clearly. There may be cases of disagreement between local, regional, and national tax authorities. At the same time, in the event of additional taxes being assessed by tax authorities, the existing amounts of fines and penalties are set at a significant amount; the amount of the fine is 80% of the amount of additional tax assessed, and the amount of the penalty on average is 18.27% per annum of the amount of additionally assessed or unpaid tax. As a result, fines and penalties may exceed the amounts of additional taxes assessed.

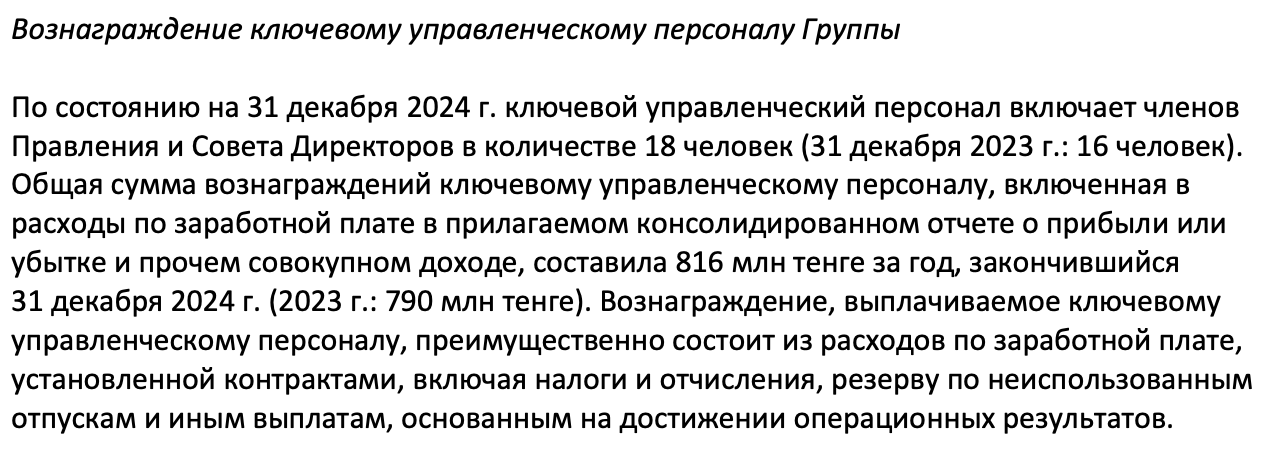

While all this was happening, key management personnel at KTZ received a total of 816 million tenge in compensation.

This includes salaries, bonuses, social benefits, and other payments. The number of executives in question is 18, which means each received an average of 45.3 million tenge.

Supreme Audit Chamber Inspection

In June 2024, the Supreme Audit Chamber (SAC) reviewed KTZ and its subsidiaries.

Auditors uncovered financial violations totaling 29 billion tenge, as well as ineffective planning and misuse of budget funds worth 168 billion tenge. Economic losses and missed profits were estimated at 307 billion tenge.

SAC Chairman Alikhan Smailov emphasized that despite around 2 trillion tenge in investment over the past four years — including 332 billion tenge from the state budget — major issues still plague the rail sector.

Smailov blamed ineffective and conservative management, as well as poorly thought-out privatization, for pushing what was once a self-sufficient company to the brink.

He urged the government and Samruq-Qazyna to urgently address KTZ’s debt load and ensure all revenues go toward restoring core assets, including renewing the main railway network.

Original Author: Ilya Astakhov

Latest news

- Two Injured Russian Climbers Rescued From Almaty Mountains

- Kazakhstan Denies Reports of Full CPC Shutdown

- South Korea to Help Kazakhstan Forecast Demographic Change

- Almaty Waste Company Stake to Return to State After Undervalued Sale

- Inspection of Former Almaty Akim’s Family Project Declared Illegal

- Kazakhstan Could Refine Russian Oil as Russia Faces Fuel Shortages

- Who Is Behind the Company Searching for Copper Near Atbasar?

- Almaty Airport to Take Out $670 Million Loan

- Kazakhstani Woman Dies in Belgrade, Father Suspects Her Friends Were Involved

- Who Will Keep Health Coverage Under Kazakhstan’s New Rules?

- Fake Journalists Tricked Karaganda Official Into Taking Out Loan

- Pavel Durov Declared a “Terrorist” in Russia

- Lawsuit Pushes Oskemen Authorities to Adopt New Alert Rules After Kazzinc Explosion

- Emergency at Pavlodar Power Plant: Two Workers Seek Medical Help

- What Back-to-School Aid Has Been Promised to Vulnerable Families?

- Employment Falls at Kazakhstan’s Small and Medium Businesses

- How Much Will It Cost to Ride Astana’s LRT From August 1?

- KASE and AIX Record Sharp Rise in Trading Activity

- Ten-Year Record: More Kazakhstanis Are Losing Their Driver’s Licenses

- What Can Tourists Expect? Kazakhstan Approves New Rules for Visitor Centers